The Classification And Normal Balance Of The Drawing Account Is:

What is the Balance Sheet?

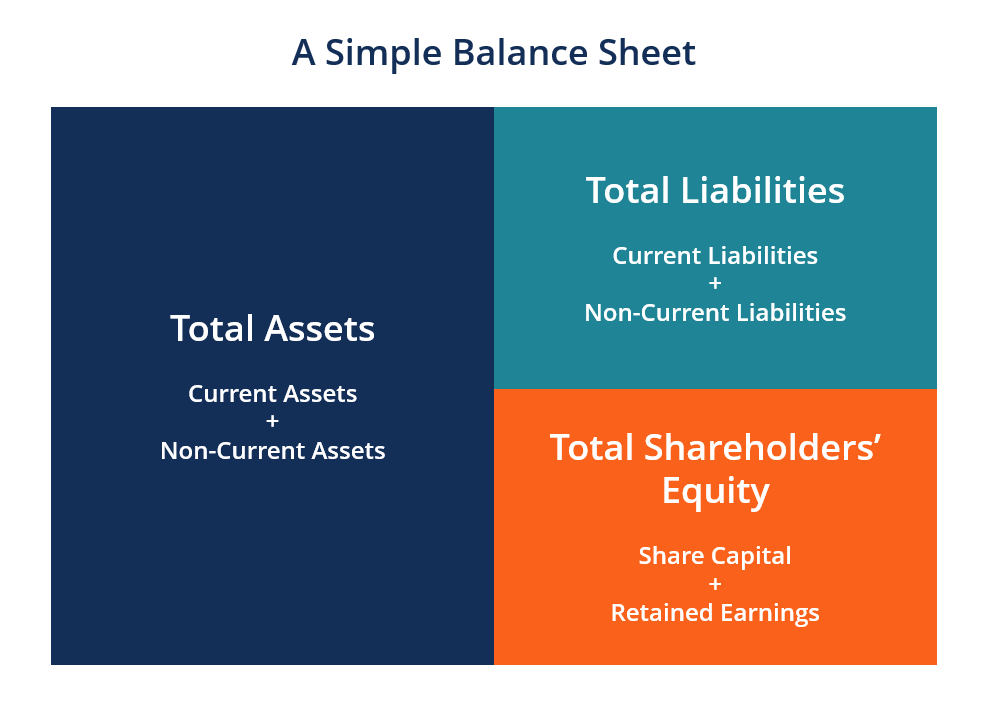

The balance sheet is one of the three fundamental financial statements Three Financial Statements The three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are and is key to both financial modeling What is Financial Modeling Financial modeling is performed in Excel to forecast a company's financial performance. Overview of what is financial modeling, how & why to build a model. and accounting. The balance sheet displays the company's total assets and how the assets are financed, either through either debt or equity. It can also be referred to as a statement of net worth or a statement of financial position. The balance sheet is based on the fundamental equation: Assets = Liabilities + Equity.

Image: CFI's Financial Analysis Course

As such, the balance sheet is divided into two sides (or sections). The left side of the balance sheet outlines all of a company's assets Types of Assets Common types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and . On the right side, the balance sheet outlines the company's liabilities Types of Liabilities There are three primary types of liabilities: current, non-current, and contingent liabilities. Liabilities are legal obligations or debt and shareholders' equity Stockholders Equity Stockholders Equity (also known as Shareholders Equity) is an account on a company's balance sheet that consists of share capital plus .

The assets and liabilities are separated into two categories: current asset/liabilities and non-current (long-term) assets/liabilities. More liquid accounts, such as Inventory, Cash, and Trades Payables, are placed in the current section before illiquid accounts (or non-current) such as Plant, Property, and Equipment (PP&E) and Long-Term Debt.

Balance Sheet Example

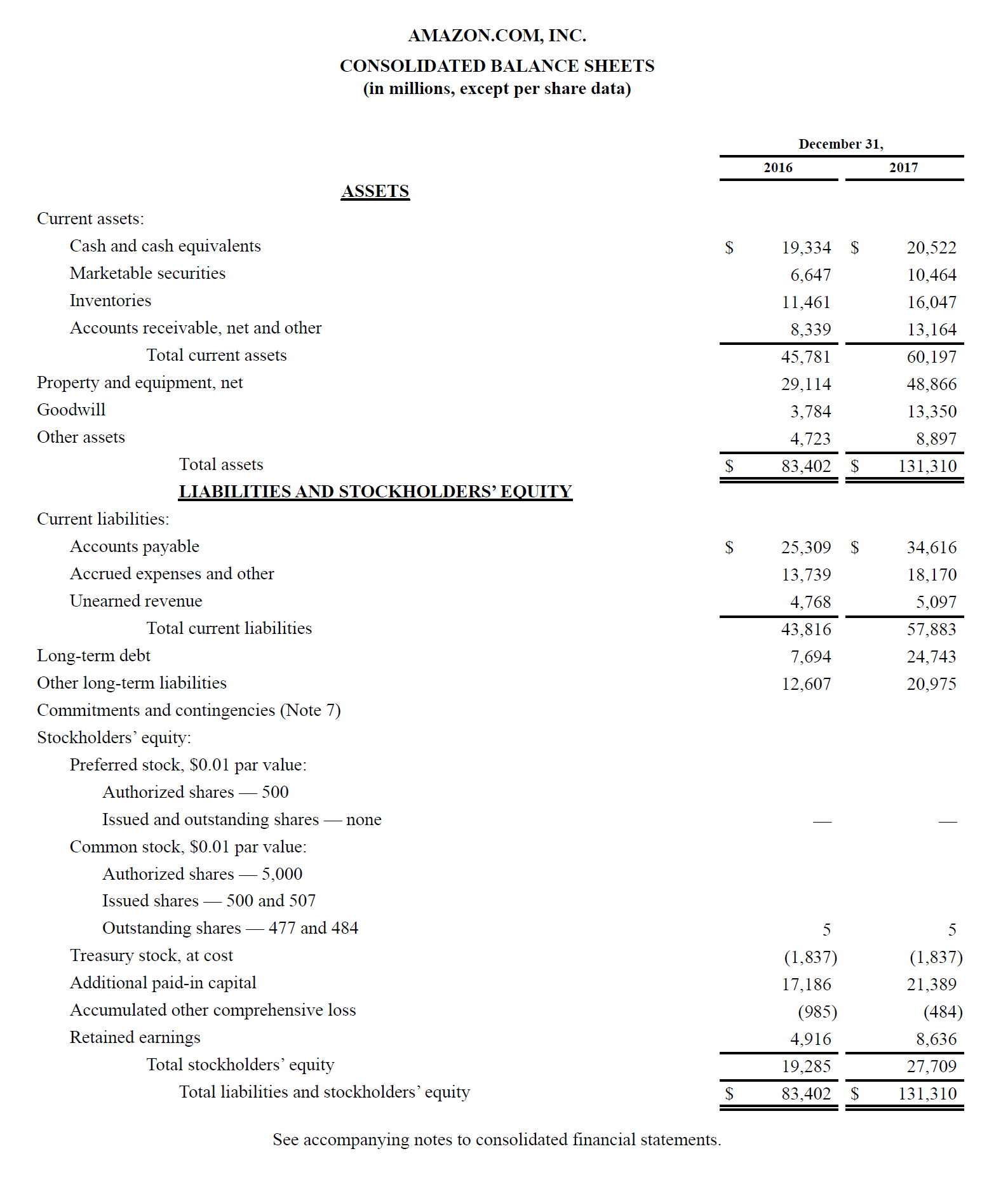

Below is an example of Amazon's 2017 balance sheet taken from CFI's Amazon Case Study Course. As you will see, it starts with current assets, then non-current assets, and total assets. Below that are liabilities and stockholders' equity, which includes current liabilities, non-current liabilities, and finally shareholders' equity.

View Amazon's investor relations website to view the full balance sheet and annual report.

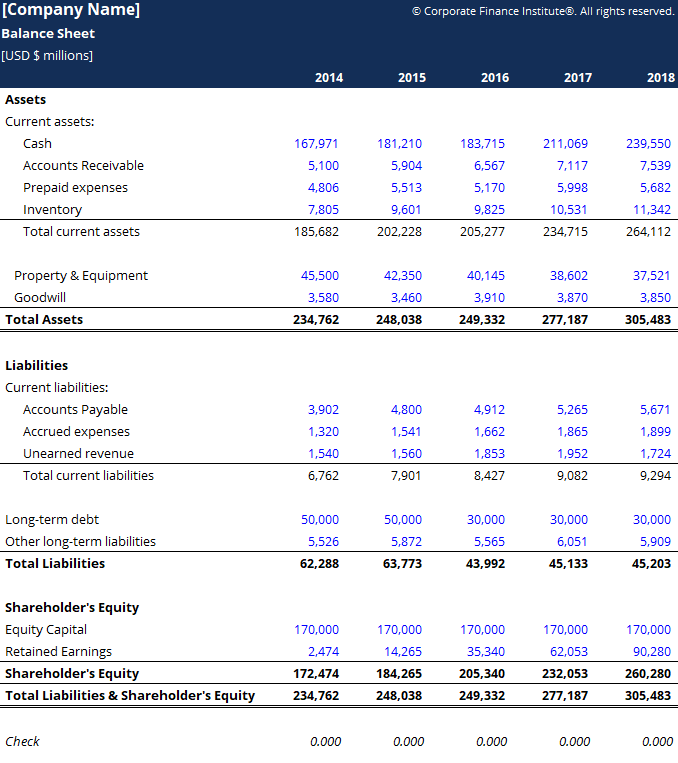

Download the Free Template

Enter your name and email in the form below and download the free template now! You can use the Excel file to enter the numbers for any company and gain a deeper understanding of how balance sheets work.

Balance Sheet Template This balance sheet template provides you with a foundation to build your own company's financial statement showing the total assets, liabilities and shareholders' equity. The balance sheet is based on the fundamental equation: Assets = Liabilities + Equity Using this template, you can add and remove line items under ea

Balance Sheet Template This balance sheet template provides you with a foundation to build your own company's financial statement showing the total assets, liabilities and shareholders' equity. The balance sheet is based on the fundamental equation: Assets = Liabilities + Equity Using this template, you can add and remove line items under ea

Balance Sheet Template

Download the free Excel template now to advance your finance knowledge!

How the Balance Sheet is Structured

Balance sheets, like all financial statements, will have minor differences between organizations and industries. However, there are several "buckets" and line items that are almost always included in common balance sheets. We briefly go through commonly found line items under Current Assets, Long-Term Assets, Current Liabilities, Long-term Liabilities, and Equity.

Learn the basics in CFI's Free Accounting Fundamentals Course.

Current Assets

Cash and Equivalents Cash Equivalents Cash and cash equivalents are the most liquid of all assets on the balance sheet. Cash equivalents include money market securities, banker's acceptances

The most liquid of all assets, cash, appears on the first line of the balance sheet. Cash Equivalents are also lumped under this line item and include assets that have short-term maturities under three months or assets that the company can liquidate on short notice, such as marketable securities Marketable Securities Marketable securities are unrestricted short-term financial instruments that are issued either for equity securities or for debt securities of a publicly listed company. The issuing company creates these instruments for the express purpose of raising funds to further finance business activities and expansion. . Companies will generally disclose what equivalents it includes in the footnotes to the balance sheet.

Accounts Receivable Accounts Receivable Accounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow

This account includes the balance of all sales revenue still on credit, net of any allowances for doubtful accounts (which generates a bad debt expense). As companies recover accounts receivables, this account decreases, and cash increases by the same amount.

Inventory Inventory Inventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a

Inventory includes amounts for raw materials, work-in-progress goods, and finished goods. The company uses this account when it reports sales of goods, generally under cost of goods sold in the income statement. Income Statement The Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or

Non-Current Assets

Plant, Property, and Equipment (PP&E) PP&E (Property, Plant and Equipment) PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,

Property, Plant, and Equipment (also known as PP&E) capture the company's tangible fixed assets. The line item is noted net of accumulated depreciation. Some companies will class out their PP&E by the different types of assets, such as Land, Building, and various types of Equipment. All PP&E is depreciable except for Land.

Intangible Assets Intangible Assets According to the IFRS, intangible assets are identifiable, non-monetary assets without physical substance. Like all assets, intangible assets

This line item includes all of the company's intangible fixed assets, which may or may not be identifiable. Identifiable intangible assets include patents, licenses, and secret formulas. Unidentifiable intangible assets include brand and goodwill.

Current Liabilities

Accounts Payable Accounts Payable Accounts payable is a liability incurred when an organization receives goods or services from its suppliers on credit. Accounts payables are

Accounts Payables, or AP, is the amount a company owes suppliers for items or services purchased on credit. As the company pays off its AP, it decreases along with an equal amount decrease to the cash account.

Current Debt/Notes Payable Current Debt On a balance sheet, current debt is debts due to be paid within one year (12 months) or less. It is listed as a current liability and part of

Includes non-AP obligations that are due within one year's time or within one operating cycle for the company (whichever is longest). Notes payable may also have a long-term version, which includes notes with a maturity of more than one year.

Current Portion of Long-Term Debt Current Portion of Long-Term Debt The current portion of long-term debt is the portion of long-term debt due that is due within a year's time. Long-term debt has a maturity of

This account may or may not be lumped together with the above account, Current Debt. While they may seem similar, the current portion of long-term debt is specifically the portion due within this year of a piece of debt that has a maturity of more than one year. For example, if a company takes on a bank loan to be paid off in 5-years, this account will include the portion of that loan due in the next year.

Non-Current Liabilities

Bonds Payable Bond Payables Bonds payable are generated when a company issues bonds to generate cash. Bonds payable refers to the amortized amount that a bond issuer

This account includes the amortized amount of any bonds the company has issued.

Long-Term Debt Debt Schedule A debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows

This account includes the total amount of long-term debt (excluding the current portion, if that account is present under current liabilities). This account is derived from the debt schedule Debt Schedule A debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows , which outlines all of the company's outstanding debt, the interest expense, and the principal repayment for every period.

Shareholders' Equity

Share Capital Share Capital Share capital (shareholders' capital, equity capital, contributed capital, or paid-in capital) is the amount invested by a company's

This is the value of funds that shareholders have invested in the company. When a company is first formed, shareholders will typically put in cash. For example, an investor starts a company and seeds it with $10M. Cash (an asset) rises by $10M, and Share Capital (an equity account) rises by $10M, balancing out the balance sheet.

Retained Earnings

This is the total amount of net income the company decides to keep. Every period, a company may pay out dividends from its net income. Any amount remaining (or exceeding) is added to (deducted from) retained earnings.

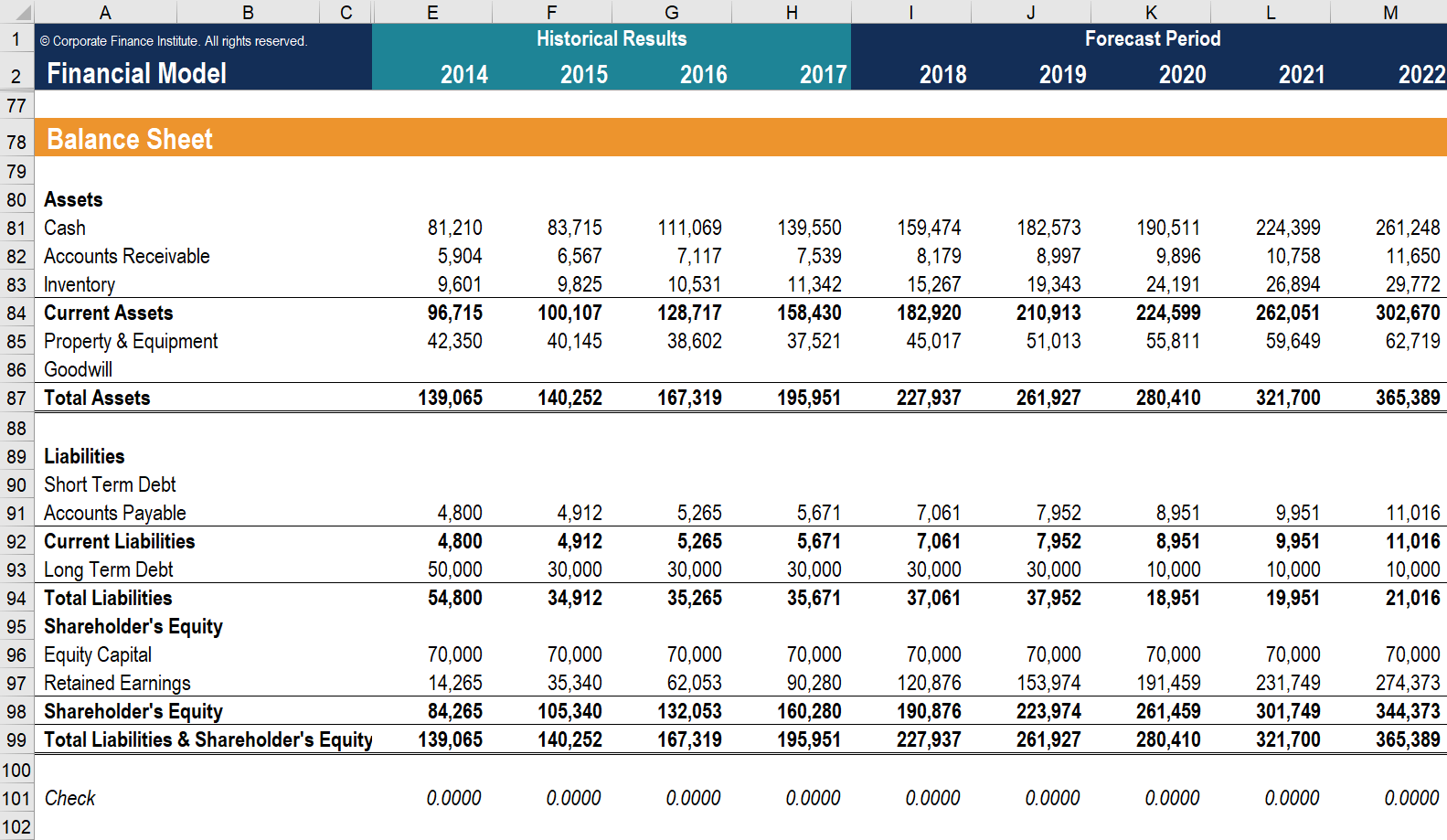

How is the Balance Sheet used in Financial Modeling?

This statement is a great way to analyze a company's financial position Analysis of Financial Statements How to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement, . An analyst can generally use the balance sheet to calculate a lot of financial ratios Leverage Ratios A leverage ratio indicates the level of debt incurred by a business entity against several other accounts in its balance sheet, income statement, or cash flow statement. Excel template that help determine how well a company is performing, how liquid or solvent a company is, and how efficient it is.

Changes in balance sheet accounts are also used to calculate cash flow in the cash flow statement Cash Flow Statement A cash flow Statement contains information on how much cash a company generated and used during a given period. . For example, a positive change in plant, property, and equipment is equal to capital expenditure minus depreciation expense. If depreciation expense is known, capital expenditure can be calculated and included as a cash outflow under cash flow from investing in the cash flow statement.

Screenshot from CFI's Financial Analysis Course.

Importance of the Balance Sheet

The balance sheet is a very important financial statement for many reasons. It can be looked at on its own and in conjunction with other statements like the income statement and cash flow statement to get a full picture of a company's health.

Four important financial performance metrics include:

- Liquidity – Comparing a company's current assets to its current liabilities provides a picture of liquidity. Current assets should be greater than current liabilities, so the company can cover its short-term obligations. The Current Ratio Current Ratio Formula The Current Ratio formula is = Current Assets / Current Liabilities. The current ratio, also known as the working capital ratio, measures the capability of a business to meet its short-term obligations that are due within a year. The ratio considers the weight of total current assets versus total current liabilities. It indicates the financial health of a company and Quick Ratio Quick Ratio The Quick Ratio, also known as the Acid-test, measures the ability of a business to pay its short-term liabilities with assets readily convertible into cash are examples of liquidity financial metrics.

- Leverage – Looking at how a company is financed indicates how much leverage it has, which in turn indicates how much financial risk the company is taking. Comparing debt to equity Finance CFI's Finance Articles are designed as self-study guides to learn important finance concepts online at your own pace. Browse hundreds of articles! and debt to total capital are common ways of assessing leverage on the balance sheet.

- Efficiency – By using the income statement in connection with the balance sheet, it's possible to assess how efficiently a company uses its assets. For example, dividing revenue by the average total assets produces the Asset Turnover Ratio Fixed Asset Turnover Fixed Asset Turnover (FAT) is an efficiency ratio that indicates how well or efficiently the business uses fixed assets to generate sales. This ratio divides net sales into net fixed assets, over an annual period. The net fixed assets include the amount of property, plant, and equipment less accumulated depreciation to indicate how efficiently the company turns assets into revenue. Additionally, the working capital cycle Working Capital Cycle The Working Capital Cycle for a business is the length of time it takes to convert the total net working capital (current assets less current shows how well a company manages its cash in the short term.

- Rates of Return – The balance sheet can be used to evaluate how well a company generates returns. For example, dividing net income by shareholders' equity produces Return on Equity Return on Equity (ROE) Return on Equity (ROE) is a measure of a company's profitability that takes a company's annual return (net income) divided by the value of its total shareholders' equity (i.e. 12%). ROE combines the income statement and the balance sheet as the net income or profit is compared to the shareholders' equity. (ROE), and dividing net income by total assets produces Return on Assets Return on Assets & ROA Formula ROA Formula. Return on Assets (ROA) is a type of return on investment (ROI) metric that measures the profitability of a business in relation to its total assets. (ROA), and dividing net income by debt plus equity results in Return on Invested Capital Return on Invested Capital Return on Invested Capital - ROIC - is a profitability or performance measure of the return earned by those who provide capital, namely, the firm's bondholders and stockholders. A company's ROIC is often compared to its WACC to determine whether the company is creating or destroying value. (ROIC).

All of the above ratios and metrics are covered in detail in CFI's Financial Analysis Course.

Video Explanation of the Balance Sheet

Below is a video that quickly covers the key concepts outlined in this guide and the main things you need to know about a balance sheet, the items that make it up, and why it matters.

As discussed in the video, the equation Assets = Liabilities + Shareholders' Equity must always be satisfied!

Learn More About the Financial Statements

To continue learning and advancing your career as a financial analyst, these additional CFI resources will be helpful:

- Income Statement Income Statement The Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or

- Current Liabilities Current Liabilities Current liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the

- Three Financial Statements Three Financial Statements The three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are

- Three Financial Statement Model 3 Statement Model A 3 statement model links the income statement, balance sheet, and cash flow statement into one dynamically connected financial model. Examples, guide

The Classification And Normal Balance Of The Drawing Account Is:

Source: https://corporatefinanceinstitute.com/resources/knowledge/accounting/balance-sheet/

Posted by: blayowle1987.blogspot.com

0 Response to "The Classification And Normal Balance Of The Drawing Account Is:"

Post a Comment